Navigating Canadian small business taxes in 2026 can feel overwhelming, but understanding the right deductions and compliance rules can save you thousands. With federal rates as low as 9% on your first $500,000 of active business income, and combined provincial rates averaging 10-13%, proper tax planning directly impacts your bottom line. This guide breaks down prorated home office deductions, vehicle expense tracking, capital cost allowance strategies, and the documentation practices that keep CRA audits at bay, helping you optimise every dollar you earn.

Table of Contents

- Understanding Canadian Small Business Tax Basics In 2026

- Maximising Deductions For Home Office And Vehicle Expenses

- Deducting Technology, Equipment, And Professional Fees Effectively

- Keeping Compliant: Record Keeping, Audits, And Avoiding Reassessment Risk

- Discover Expert Tax Support With Taxfiyer In 2026

Key takeaways

| Point | Details |

|---|---|

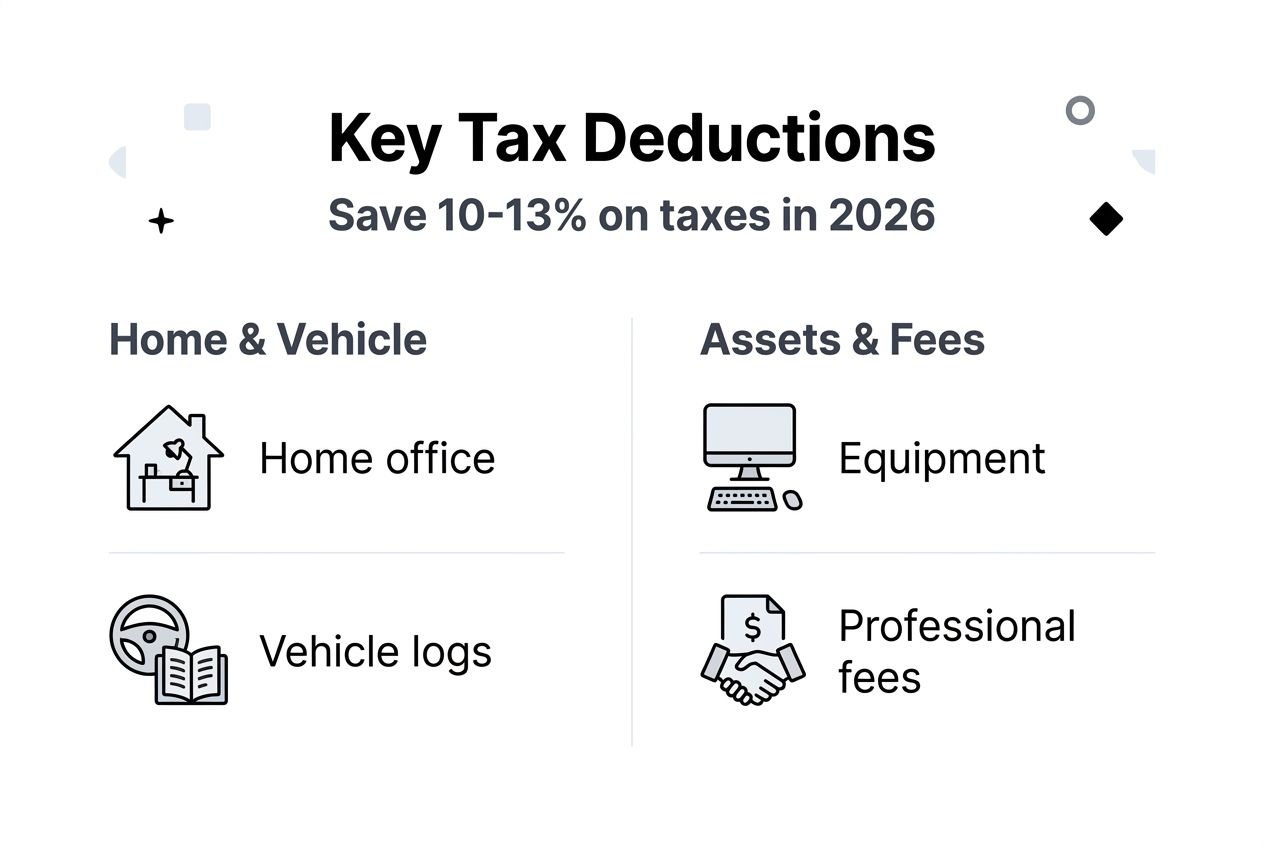

| Master home office and vehicle deductions | Claim prorated workspace costs and track mileage meticulously to maximise legitimate deductions without triggering audits. |

| Leverage the Small Business Deduction strategically | Federal rates drop to 9% on the first $500,000 of active income, but phase out as taxable capital approaches $15 million. |

| Use capital cost allowance for equipment | Spread technology and furniture costs over time through CCA, with accelerated options for computers and software. |

| Maintain bulletproof documentation | Detailed receipts, mileage logs, and invoices prevent reassessments and protect against penalties up to a decade later. |

| Consult professionals for complex structures | Associated corporations and capital thresholds require expert guidance to avoid costly mistakes and maximise tax savings. |

Understanding Canadian small business tax basics in 2026

Canadian Controlled Private Corporations enjoy significant tax advantages when structured properly. For the fiscal year ending March 2026, the federal rate is 9% on the first $500,000 of active business income, a dramatic reduction from the standard 38% corporate rate. Combined with provincial rates, most small businesses pay between 10-13% total tax on income within this threshold.

The Small Business Deduction provides this preferential treatment, but comes with specific limitations. Business limits phase out when taxable capital reaches $10 million, disappearing entirely at $15 million. This capital test includes assets like investments, equipment, and property, not just cash reserves.

Associated corporations present additional complexity. When businesses share common ownership or control, they must split the $500,000 business limit among all entities. This prevents income splitting schemes but requires careful planning when expanding operations or partnering with family members. Understanding these foundational rules prevents costly surprises during filing season.

Key elements affecting your 2026 tax position include:

- Active business income versus investment income classification

- Taxable capital calculations including loans and shareholder advances

- Association rules affecting multi-corporation structures

- Provincial variations in small business rates and thresholds

- Income thresholds triggering additional tax obligations

Working with Montreal accountant and tax services professionals ensures you navigate these rules correctly from the start. Proper structure and classification decisions made early compound into significant savings over time.

Maximising deductions for home office and vehicle expenses

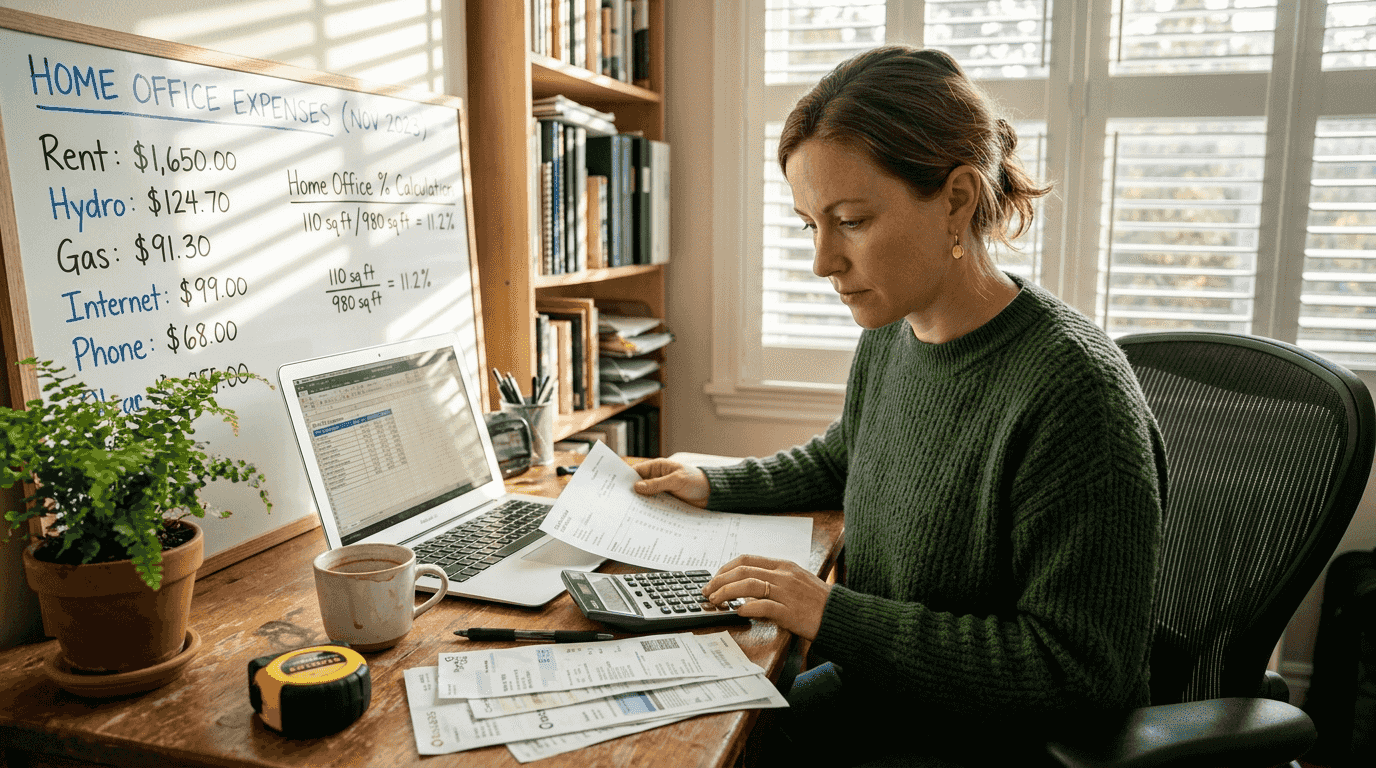

Home office deductions represent one of the most valuable yet frequently misunderstood tax benefits. Calculate your deduction by measuring dedicated workspace square footage as a percentage of total home size. If your office occupies 150 square feet in a 1,500 square foot home, you can claim 10% of eligible expenses.

CRA allows prorated deductions for utilities, mortgage interest, property taxes, rent, insurance, and internet costs. The space must be used exclusively and regularly for business, or serve as your principal place of business. Meeting clients at home strengthens your claim even if you work elsewhere occasionally.

Vehicle expenses require meticulous tracking but deliver substantial savings. Detailed mileage logs recording date, destination, purpose, and kilometres driven establish business use percentage. If business trips represent 60% of total mileage, you can claim 60% of all vehicle costs including fuel, repairs, insurance, licence fees, parking, and capital cost allowance on the vehicle itself.

| Expense category | What qualifies | Documentation needed |

|---|---|---|

| Home office | Utilities, internet, rent, mortgage interest, property tax, insurance | Floor plan, square footage calculation, receipts |

| Vehicle | Fuel, repairs, insurance, parking, lease payments, CCA depreciation | Mileage log, fuel receipts, repair invoices |

| Workspace supplies | Furniture, computers, phones dedicated to business use | Purchase receipts, business use justification |

Pro Tip: Create a simple spreadsheet for vehicle tracking with columns for date, start location, end location, business purpose, and kilometres. Snap photos of your odometer at year start and end for verification. This 30 second daily habit protects thousands in deductions.

Many business owners underestimate legitimate claims or lack proper records. Tax professional services help identify overlooked deductions while ensuring documentation meets CRA standards, maximising your refund without audit risk.

Deducting technology, equipment, and professional fees effectively

Capital assets like computers, office furniture, and equipment cannot be fully expensed in year one. Instead, capital cost allowance lets you deduct a percentage annually over the asset's useful life. Different asset classes have different CCA rates, ranging from 20% for general equipment to 55% for certain computer hardware.

Computer software and hardware often qualify for accelerated depreciation rates, letting you recover costs faster. The half year rule typically applies to new purchases, limiting first year claims to 50% of the normal CCA rate. Understanding which class each asset falls into optimises your deduction timing.

Professional fees represent fully deductible current expenses. Legal advisors, tax accountants, and consultants provide services recognised as necessary business costs by CRA. Unlike capital purchases, you deduct the full amount in the year paid, providing immediate tax relief.

Strategic timing of equipment purchases and professional service payments can shift deductions between tax years. If your income fluctuates, accelerating or deferring certain expenses optimises your effective tax rate. This requires planning throughout the year, not just at year end.

Common technology and equipment deductions include:

- Desktop computers, laptops, and tablets used exclusively for business operations

- Office furniture including desks, chairs, filing cabinets, and shelving units

- Specialised equipment specific to your industry or service delivery

- Software subscriptions and licences for business management and productivity tools

- Phones, printers, scanners, and other peripheral devices supporting operations

Pro Tip: Maintain a fixed asset register tracking purchase date, cost, CCA class, and accumulated depreciation for each capital item. This simplified schedule makes year end filing straightforward and supports your claims if questioned. Spreadsheet templates are available free online or through tax professional consultation services.

Regular equipment review identifies fully depreciated assets that can be disposed of, clearing your records while potentially generating small capital losses. Professional guidance ensures you apply CCA rules correctly, especially for partial year purchases or mixed use assets.

Keeping compliant: record keeping, audits, and avoiding reassessment risk

Documentation separates legitimate deductions from rejected claims. CRA requires expenses to be reasonable, incurred to earn business income, and properly supported by evidence. Receipts must show date, amount, vendor, and description of goods or services purchased. Digital copies are acceptable if clearly legible and securely stored.

Mileage logs need date, starting point, destination, business purpose, and distance for every trip claimed. Reconstruction from memory during an audit rarely succeeds. Contemporary records created at the time of travel carry far more weight than spreadsheets compiled months later.

CRA can reassess returns for three years after initial assessment under normal circumstances. Negligent documentation triggers reassessments up to a decade later, with penalties and potential shareholder liability as seen in recent Tax Court rulings. Gross negligence penalties reach 50% of understated tax, plus interest compounding from the original filing date.

Best practices for bulletproof compliance include:

- Digitising receipts immediately using smartphone apps that timestamp and categorise expenses

- Maintaining separate business bank accounts and credit cards for clean transaction records

- Logging mileage in real time using GPS tracking apps designed for tax purposes

- Storing documentation for seven years as recommended by CRA for audit protection

- Conducting quarterly reviews to identify missing receipts while memories are fresh

Accounting software automates much of this tracking, categorising expenses and flagging unusual patterns. Cloud based systems provide automatic backups and multi device access, eliminating lost paperwork excuses.

"The court found the corporation's lack of contemporaneous documentation and reasonable explanation for shareholder transactions constituted gross negligence, upholding CRA's decade late reassessment and substantial penalties. Proper record keeping is not optional, it's your first line of audit defence."

Audit triggers include dramatic year over year expense changes, unusual expense ratios compared to industry norms, and round numbers suggesting estimates rather than actual costs. Consistent, detailed records across multiple years demonstrate good faith compliance even if specific claims are questioned.

Professional tax compliance services establish systems that work with your workflow, not against it. Initial setup investment pays dividends through stress free filing seasons and audit protection lasting years. Many business owners discover previously overlooked deductions once proper tracking reveals actual expense patterns.

Discover expert tax support with TaxFiyer in 2026

Maximising your small business deductions while maintaining CRA compliance demands expertise and time most entrepreneurs lack. TaxFiyer's Montreal based team of CPAs specialises in Canadian small business taxation, combining deep regulatory knowledge with practical strategies tailored to your specific situation.

Our comprehensive approach covers strategic tax planning throughout the year, not just scrambling at deadline. We identify deduction opportunities you're missing, structure transactions to optimise tax treatment, and maintain documentation systems that withstand scrutiny. From initial business setup through growth phases and eventual succession planning, we're your year round financial partner.

Bilingual service in English and French ensures clear communication of complex concepts. Most returns are completed within 48 hours, with transparent pricing and guaranteed maximum refunds. When CRA correspondence arrives, our representation services handle communications directly, protecting your time and interests.

Schedule your free consultation with Montreal accountant and tax services to discover how much you could be saving in 2026. Our track record speaks for itself, thousands recovered for clients through proper deduction claims and strategic planning.

FAQ

What expenses can small businesses deduct in Canada?

Home office costs prorated by workspace size, vehicle expenses supported by mileage logs, technology and equipment through capital cost allowance, and professional service fees are commonly deductible. All expenses must be reasonable, properly documented, and incurred specifically to earn business income. Personal portions of mixed use items cannot be claimed.

How does the small business deduction affect my corporate tax rate?

The deduction reduces federal tax from 38% to 9% on your first $500,000 of active business income, with combined federal and provincial rates typically totalling 10-13%. This preferential rate phases out when taxable capital exceeds $10 million, disappearing completely at $15 million. Associated corporations must share the $500,000 threshold among all related entities.

What records do I need to keep to avoid tax audit issues?

Maintain detailed receipts showing date, vendor, amount, and business purpose for all expenses claimed. Vehicle deductions require contemporaneous mileage logs with date, destination, business reason, and kilometres for each trip. Keep documentation for at least seven years, store digital backups securely, and use accounting software to organise transactions by category for easy retrieval during reviews.

When should I consult a tax professional about my small business?

Consult professionals when incorporating your business, establishing multi corporation structures, facing CRA audits or reassessments, or when your taxable capital approaches $10 million. Complex situations like associated corporation rules, income splitting strategies, and capital gains exemptions require expert guidance to avoid costly mistakes. Annual reviews ensure you're optimising deductions and maintaining compliance as rules change.